The "special" 2.99% interest rate at the dealership might actually be the most expensive way to drive away in your new CX-5. It sounds counterintuitive, but the convenience of on-the-spot mazda finance often comes with a hefty side of hidden fees and rigid terms that don't suit your actual lifestyle. While a low headline rate looks great on a showroom poster, the real cost is often buried in the fine print of your contract.

We understand the pressure of sitting in that glass office, feeling like you have to sign for Mazda Assured just to get the deal done. You want lower monthly repayments and total transparency, not a $912 dealer agency fee or a $395 establishment fee tucked away where you won't notice. This article promises to show you exactly how to secure the best rates for your new or used Mazda by pitting dealer offers against independent brokerage solutions.

We will compare current 2026 interest rates, demystify Guaranteed Future Value (GFV) terms, and reveal how a tailored loan provides the flexibility that "one-size-fits-all" dealer contracts simply can't match. By the end, you will have the confidence to organise a loan that puts your budget first, not the dealer's bottom line.

• Discover how a broker’s access to over 30 lenders creates the competition needed to drive down your interest rates compared to a single dealer offer.

• Understand the real-world difference between mazda finance GFV products and standard loans, focusing on how each affects your ownership at the end of the term.

• Identify the hidden "doc" and agency fees that often lurk in dealer contracts, ensuring you only pay for the finance you actually need.

• Learn how to position yourself as a "cash buyer" at the dealership to unlock better discounts on the vehicle price itself.

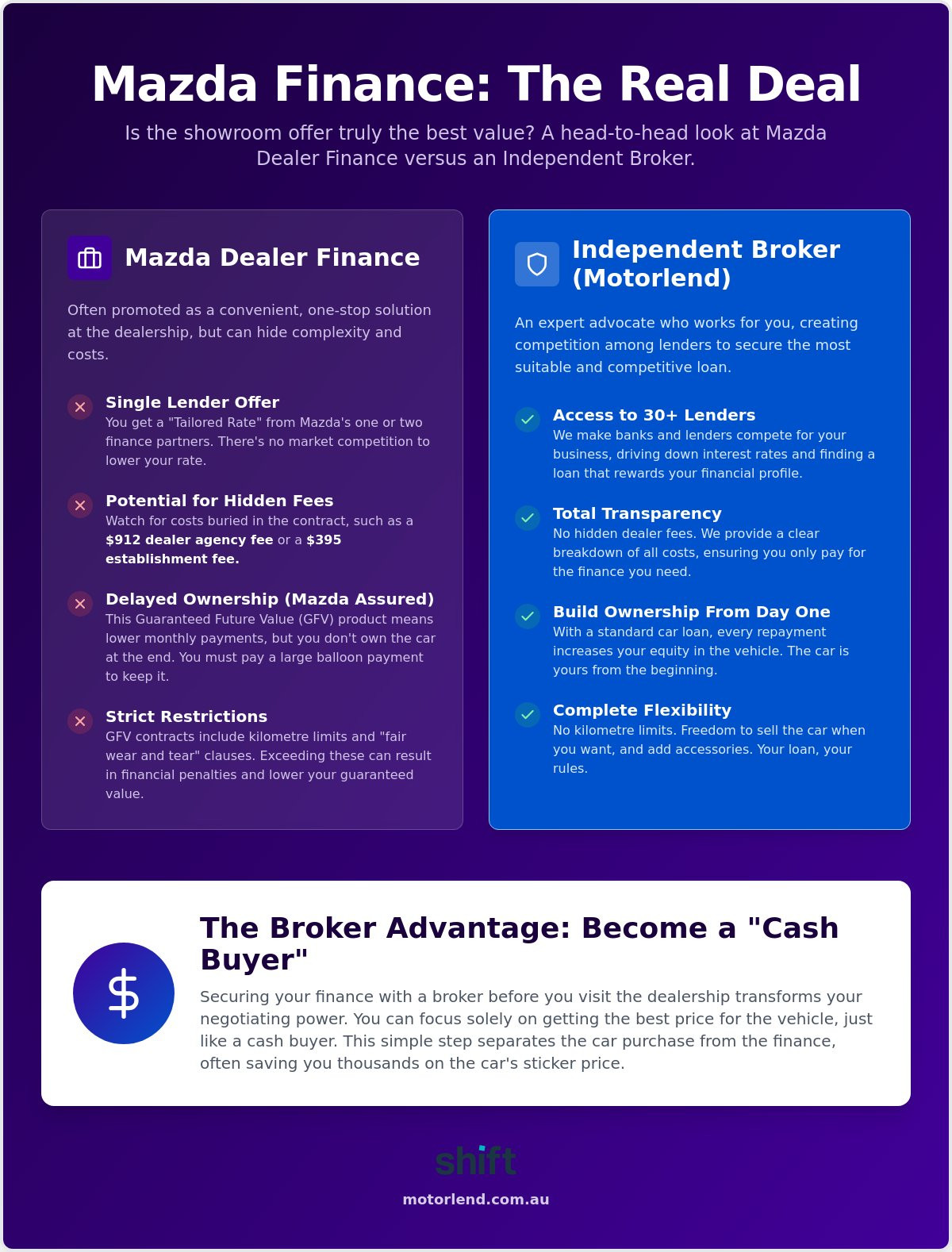

Buying a Mazda is an exciting milestone, but the finance part often feels like a high-pressure sales pitch. When we talk about mazda finance, it is actually a choice between two distinct paths. You can go with the manufacturer-backed loans offered in the showroom or choose an independent brokerage solution. Most Australians don't realise they aren't restricted to the dealer's office just because they've fallen in love with a car on the lot.

In the current 2026 market, dealer finance typically falls into two categories. First, there is the traditional Fixed Rate Car Loan. This offers predictable monthly repayments over a set term. Second, there is Mazda Assured, which is a Guaranteed Future Value (GFV) product. These are often structured as hire purchase agreements where you pay less during the loan term but face a large "balloon" payment at the end to keep the car. It's a popular choice for those who like to upgrade every few years, but it requires careful management of your kilometres and car condition.

Dealers now use a "Tailored Rate" system. This means the interest rate you are offered isn't a flat number on a poster. It is calculated specifically for you based on your credit score, loan term, and deposit. If your credit history isn't perfect, that "from" rate you saw online might disappear quickly. This is where staying independent gives you a massive advantage.

Dealerships generally prioritise financing for new and demonstrator models. They want to move current stock, so their best promotional rates are almost always tied to the latest 2025 or 2026 models. If you are looking at an older used Mazda or a private sale, the dealer's interest often fades. Independent brokers fill this gap perfectly. We provide the same level of support whether you are buying a brand-new CX-90 from a showroom or a well-kept 2021 Mazda3 from a private seller in the next suburb over.

A broker acts as your personal advocate in the lending market. While a dealer only has access to one or two captive lenders, a broker like Motorlend compares options from over 30 different banks and specialist lenders. This competition is what drives your interest rate down. We look at your specific profile to find a lender that rewards your situation, rather than forcing you into a rigid dealer box. You can explore our full range of Vehicle Finance solutions to see how we tailor loans for every type of buyer.

Choosing between Mazda Assured and a standard car loan is about more than just the monthly figure. While Mazda Assured is the flagship product for mazda finance, it is designed to keep you in a cycle of new car upgrades. It promises lower repayments today, but there is a trade-off. You are essentially paying for the depreciation rather than building equity in the vehicle. At the end of the term, you don't own the car outright unless you settle a significant balloon payment, which can often be a shock to your long-term budget.

Standard principal-and-interest loans through an independent lender work differently. You build ownership from day one. Every payment you make increases your stake in the car. This distinction is a key part of the CHOICE guide to car finance options, which points out that having an independent offer in your pocket is the best way to benchmark what the dealer is telling you. If you want to own your Mazda for the next decade, the "convenience" of GFV might actually cost you more in the long run.

Mazda Assured comes with strict fine print that acts like a set of golden handcuffs. You must commit to a pre-agreed kilometre limit at the start of the contract. If your lifestyle changes and you start driving more, you face per-kilometre penalties at the end of the term. There are also "fair wear and tear" requirements that can be subjective. If the dealer decides a small dent or scratch exceeds their guidelines, your guaranteed value drops instantly. It is a lease-style structure that suits some, but for high-mileage drivers, it can be a financial trap.

Independent loans don't care how many kilometres you rack up or if you want to add aftermarket accessories like a tow bar or roof racks. You have the freedom to choose your own term, typically between one and seven years, without manufacturer restrictions. This flexibility allows you to sell the car whenever you like without navigating complex GFV exit clauses. For a deeper look at structuring your debt correctly, read our Car Finance: The Complete 2026 Guide to Stress-Free Lending. If you want to see how your numbers stack up right now, you can start a quick application online to compare your options.

Don't let a shiny headline rate distract you from the bottom line. When you are looking at mazda finance options, the interest rate is only half the story. To find the true cost of your loan, you need to look at the fees that the dealership might not mention during the initial walk-around. Between establishment fees and monthly service charges, the amount you actually pay back can climb much higher than you first thought.

In the 2026 Australian market, Mazda Finance consumer loans often include a $395.00 establishment fee and a significant $912.25 dealer agency fee. On top of that, you might see an $8.00 monthly account administration fee. These costs add up quickly. A broker helps you cut through this by providing a transparent breakdown of every cent, ensuring your monthly budget stays on track without nasty surprises.

The comparison rate is the only number that truly matters for Mazda buyers because it combines the interest rate and most upfront and ongoing fees into a single percentage. While a dealer might promote a low "headline" rate to get you through the door, the comparison rate reveals the mathematical reality of the deal. If there is a large gap between these two numbers, it means the contract is heavy on hidden fees that are being baked into your monthly repayments.

Low-rate dealer finance is often a marketing tool rather than a genuine discount. If you accept a "Zero Percent" or heavily subsidised rate, the dealer is less likely to budge on the car's purchase price. They need to make their margin somewhere. By choosing independent finance, you can negotiate the car price as a "cash buyer" and then secure a competitive loan separately. This often results in a lower total cost of ownership. For used car buyers, it is even more critical to watch for extra charges; learn more in our guide on Dealer Administration Fees on Used Cars: What to Avoid.

Your credit score also dictates the "Tailored Rate" you receive at the dealership. If your score isn't in the top tier, your offered rate could jump significantly from the advertised starting point. We believe you should know your real numbers before you step onto the lot. To see exactly what you qualify for without the showroom pressure, get your personalised rate quote today.

Settling for the first mazda finance offer you see in a showroom is like buying a car without checking the price tag. While a dealer is limited to a single captive lender, a broker works as your personal negotiator. We compare options from over 30 different banks and specialist lenders to find the one that actually wants your business. This competition is the secret to driving down your interest rate and finding terms that don't feel like a compromise.

One of the biggest advantages of independent finance is the "cash buyer" status it gives you. When you walk into a dealership with your pre-approval already sorted, the power dynamic shifts in your favour. You aren't there to haggle over confusing monthly repayments or balloon percentages. Instead, you can focus entirely on the drive-away price of the car. Dealers are often more willing to offer a genuine discount when they know your funding is already secure and ready to go.

Speed is another area where modern brokers now outpace the old showroom model. You don't need to spend your Saturday sitting in a glass office while a salesperson "checks with the manager." Our digital-first approach means we can often match or beat dealership turnaround times, getting you behind the wheel of your new Mazda without the unnecessary stress or paperwork.

For sole traders and companies eyeing a Mazda BT-50 for the job site or a CX-90 for the executive fleet, the right loan structure is vital for your tax strategy. We specialise in tailoring chattel mortgages and hire purchase agreements that align with your business cash flow. Unlike a dealer who might offer a generic consumer product, we focus on the specific needs of business owners. You can explore our dedicated Commercial Finance options to see how we can help your bottom line.

The smartest way to buy a car is to have your finance organised before you even step onto the lot. Pre-approval gives you a clear budget ceiling and the confidence to walk away if the dealer's deal doesn't stack up. It takes the guesswork out of the process and puts you firmly in the driver's seat. Ready to see how much you could save compared to the showroom offer? Head over to the Motorlend Application Page to start your comparison and get a personalised quote in minutes.

Securing the right mazda finance is about more than just matching a monthly repayment to your budget. It's about ensuring you have the flexibility to drive where you want, modify your car as you please, and avoid the "balloon" surprises that often hide in dealership contracts. By looking beyond the showroom floor, you've already taken the first step toward a more transparent and cost-effective way to own your next vehicle.

You don't have to navigate the fine print alone. Our team of expert brokers handles all the paperwork for you, providing access to a wide panel of leading Australian lenders to ensure you get a deal that actually fits your life. Whether you are eyeing a brand-new BT-50 for work or a well-kept used CX-5 for the family, we specialise in fast approvals that put you back in control of the negotiation.

Stop guessing and start comparing. Apply for tailored Mazda finance with Motorlend today and experience a faster, simpler way to get on the road. Your perfect Mazda is waiting; let's make sure the finance is just as impressive as the drive.

Yes, you can definitely finance a private sale, though you will need to look beyond the dealership to do it. While manufacturer-backed finance is usually tied to showroom stock, an independent broker can organise a loan for a used Mazda bought from any private seller across Australia. This gives you the freedom to hunt for the best deal on the car itself without worrying about how to fund it.

Mazda Assured sets a minimum value for your car at the end of the loan term, provided you meet strict kilometre and fair wear and tear conditions. You pay lower monthly instalments during the term, but you will face a large balloon payment if you want to keep the car at the end. It is a popular choice for those who upgrade every few years, but it can be restrictive for high-mileage drivers who don't want to be penalised for extra travel.

A broker is generally the smarter choice because they compare over 30 lenders to find the most competitive rate for your specific profile. Dealers only offer one or two captive options and often bundle in high agency fees. By using a broker, you walk into the dealership as a "cash buyer," which gives you much more bargaining power to negotiate a lower price on the actual vehicle.

There isn't one "magic" number, but your credit score directly determines the "Tailored Rate" a dealer will offer you. While those with scores above 700 usually secure the best promotional rates, an independent broker can still find competitive solutions for those with average or building credit. We look at your whole financial picture to find a lender that rewards your current situation rather than just a single number.

This depends entirely on your specific contract, as some dealer loans include heavy break costs for early exit. Many independent car loans offered through a broker allow for extra repayments or early payouts with minimal or even zero fees. Always check the comparison rate and the fine print regarding "early termination" before you sign, as this flexibility can save you thousands in interest over the life of the loan.