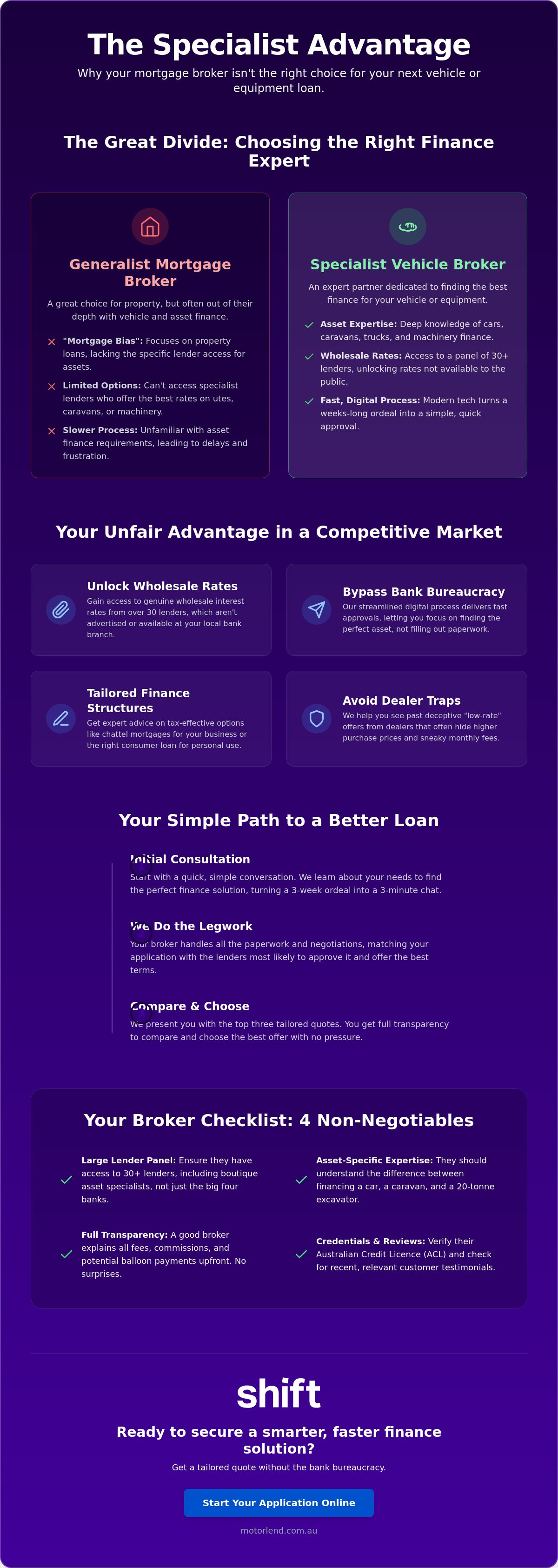

Your local mortgage broker might be a legend at securing home loans, but asking them to fund your new ute or caravan is like asking a plumber to fix your laptop. Most generalist brokers suffer from a "mortgage bias," meaning they often lack the specific lender access required to find the best deal on wheels or heavy equipment. Choosing the right vehicle finance broker is the difference between getting stuck with a high-interest dealership offer and securing genuine wholesale rates that keep your cash in your pocket.

We know the drill. You're likely fed up with confusing financial jargon, slow bank approvals, and the fear of hidden balloon payments lurking in the fine print. It should be an exciting time, not a mountain of paperwork. This guide simplifies the entire process. You'll learn how to identify a true asset specialist, what questions to ask to ensure transparency, and how to fast-track your application. We're stripping away the stress so you can focus on the drive, with a contract that's clear, fair, and tailored to your needs.

• Learn why choosing a specialist vehicle finance broker is vital for securing better rates than a generalist mortgage broker or a big bank.

• Discover how to unlock genuine wholesale rates that aren't available to the general public through a wide panel of lenders.

• Understand the step-by-step process of organising your loan, from the initial consultation to comparing the top three tailored quotes.

• Identify common dealer traps and low-rate offers that often hide a much higher purchase price and sneaky monthly fees.

• Find out how to bypass bank bureaucracy to secure fast approvals for everything from a new family caravan to heavy business machinery.

The finance world has shifted, and in 2026, the old way of begging a bank for a loan is dead. If you've ever wondered What is a Vehicle Finance Broker, the answer is simple. They are professional intermediaries who negotiate between you and a massive panel of lenders to find the best deal. Instead of being stuck with whatever "special" your local branch is running, you get access to the whole market. A finance broker is an expert who organises tailored lending solutions by comparing dozens of credit providers.

Modern, digital-first brokers use advanced technology to strip away the traditional bank bureaucracy. We're talking about automated document verification and real-time lender matching that turns a three-week ordeal into a three-minute conversation. It's about speed and precision. You get the fast approval you need for that new ute or caravan without the headache of printing, scanning, and signing a mountain of paperwork. Banks only offer their own products, but a broker offers genuine choice.

The biggest myth in finance is that going direct to your bank saves you money. It's usually the opposite. Banks are limited to their own products, which means they'll never tell you if a competitor has a lower rate or better terms. Working with a vehicle finance broker gives you several distinct advantages:

Access to interest rates that aren't advertised to the general public or available at your local branch.

Expert knowledge of vehicle finance structures like chattel mortgages for business owners or consumer loans for individuals.

Your broker handles the hours of paperwork and phone calls while you focus on finding the right car, boat, or excavator.

Choosing a specialist ensures your application is sent to the lender most likely to approve it the first time. This protects your credit score and gets you behind the wheel faster. It's about having a partner who knows the market and works for you, not the bank.

Don't fall for the "one-size-fits-all" trap. Buying a daily driver, a weekend caravan, or a 20-tonne excavator requires vastly different financial approaches. A generalist broker might be great at mortgages, but they often lack the deep lender relationships needed for niche assets. You need a vehicle finance broker who understands the specific credit criteria for the gear you actually want to buy. If they spend all day talking about offset accounts and LVRs, they probably aren't the right fit for your truck or boat.

Start by checking their lender panel. A top-tier vehicle finance broker should have access to 30 or more lenders. This list must include boutique asset specialists, not just the big banks. Transparency is also non-negotiable. Your broker should explain fees, commissions, and those potentially nasty balloon payments before you ever put pen to paper. If you're ready to see what's possible, you can start your application online in just a few minutes.

Securing caravan finance is a different beast compared to a standard car loan. Lenders look at different risk profiles for leisure assets and often have specific age limits on the unit. For business owners, the nuances get even deeper. You need to understand tax-effective structures like chattel mortgages or leasing. These ABN-specific options can significantly impact your cash flow and EOFY position, so your broker needs to know their way around a balance sheet.

Always verify that your broker holds an Australian Credit Licence (ACL) or is an authorised representative. This ensures you're protected by Australian regulations and professional standards. Don't just take their word for it. Look for recent customer testimonials that specifically mention vehicle or commercial finance deals. If their reviews are entirely about home loans, they might lack the specific "runs on the board" required for complex equipment needs.

Forget the multi-week slog associated with home loans. A specialist vehicle finance broker operates on a much faster timeline, often moving from initial chat to settlement in just 24 to 48 hours. The process is designed to be lean, digital, and entirely focused on getting you behind the wheel without the usual bank-induced headaches.

We discuss your budget, the specific asset type, and your long-term goals. This ensures the loan structure matches your cash flow.

Your broker scouts their panel and presents the top three options tailored to your credit profile. You see the rates and fees side-by-side.

This is where you provide your payslips, bank statements, and ID. Everything is submitted digitally to keep the momentum going.

The broker manages the back-and-forth with the lender's credit team. Once approved, they coordinate with the seller to ensure the funds land exactly where they need to.

Ready to get the ball rolling? You can start your application online right now and have a specialist reviewing your options today.

The secret to a same-day submission is organisation. If you are applying for a personal loan for a car or caravan, you will typically need two recent payslips and a copy of your driver's licence. For business equipment, lenders will want to see your recent tax returns or an ABN confirmation. Keep these files as clear PDFs on your phone or computer. This allows your vehicle finance broker to hit the "submit" button the moment you choose a lender, bypassing the usual back-and-forth delays.

Walking into a dealership with a pre-approval is like carrying cash. It completely changes the power dynamic at the car yard or boat show. You aren't just another browser; you are a "ready-to-buy" customer with the backing of a major lender. Once you find the right asset, your broker takes over again. They coordinate directly with the vendor to finalise the invoice and payment details, so you only need to show up and collect the keys.

Don't get blinded by a flashy interest rate. A low percentage is only one part of the puzzle. To truly save money, you must look at the "Total Cost of Credit." This includes establishment fees and ongoing monthly charges that can quietly add thousands to your debt. A transparent vehicle finance broker will show you the comparison rate, which factors in these costs to give you the real story. In 2026, ASIC has made misconduct in the car finance sector a top priority, specifically targeting excessive fees, so it pays to have a broker who values honesty over a quick commission.

Watch out for those "0% interest" offers at the dealership. These are often marketing traps where the interest is simply "front-loaded" into a higher purchase price for the vehicle. You lose your power to negotiate a better deal on the car or caravan itself. By securing your own finance first, you can walk onto the lot as a cash buyer and hunt for the lowest drive-away price. You can also tailor your repayments to suit your life. Aligning your loan with your weekly or fortnightly pay cycle keeps your budget on track and avoids that end-of-month stress.

A specialist also helps you future-proof your financial position. They ensure your loan term and any balloon payments match the expected resale value of your asset. This means when it's time for a business expansion or a caravan upgrade in a few years, you aren't stuck with a debt that's worth more than the vehicle.

We're different because we don't do mortgages. While other brokers are bogged down in home loan paperwork, we live and breathe vehicle, leisure, and equipment finance. We understand that when you want a new bike, boat, or excavator, you want it now. Our digital-first approach means fast, no-nonsense approvals without the bank-style bureaucracy. You get direct access to experts who speak your language and value your time. Apply for your asset finance online in minutes and experience a faster way to get moving.

Choosing the right vehicle finance broker is about more than just finding a low interest rate; it's about finding a partner who understands the Australian asset landscape. You now know how to spot the "mortgage bias" of generalist brokers and why avoiding dealer finance traps can save you thousands over the life of your loan. By focusing on asset-specific expertise and a transparent digital process, you can bypass bank delays and secure the wholesale rates you deserve.

At Motorlend, we don't do mortgages. We live and breathe vehicle and commercial assets, providing you with direct access to a wide panel of leading Australian lenders. Our fast, digital-first approval process is designed for speed, ensuring you spend less time on paperwork and more time enjoying your new ute, boat, or machinery. Don't let bank bureaucracy slow you down. Get a quick quote for your next vehicle with Motorlend today and see how easy asset finance can be. Your next adventure is just a few clicks away.

Most brokers earn their income through commissions paid by the lender, though some may charge an establishment fee typically ranging from $200 to $1,000. These costs are generally built into the total loan amount, so you won't have to pay anything out of pocket upfront. A transparent vehicle finance broker will always disclose these fees in your initial quote so there aren't any surprises later.

You can usually expect a formal approval within 24 to 48 hours when working with a specialist. Because digital-first brokers use automated document verification and have direct access to credit assessors, they move much faster than traditional banks. This speed is essential in the current Australian market where popular utes and caravans often sell within days of being listed.

Yes, brokers specialise in finding solutions for Australians who don't fit the rigid "perfect credit" box of the big banks. They have access to a wide panel of lenders, including those who look at your current income and bank statements rather than just a past credit score. Whether you have a previous default or an irregular income as a contractor, a broker knows which lender is most likely to say yes.

The primary difference is their area of expertise and the lenders they work with. A mortgage broker handles long-term property debt, while a vehicle finance broker focuses on shorter-term loans for depreciating assets like cars, boats, and heavy machinery. The credit criteria for a five-year car loan are vastly different from a thirty-year home loan; even for products in other markets like homeowner loans UK, using a specialist ensures you get the best structure for your asset.

Absolutely, and using a broker is often the safest way to fund a private purchase. They handle the essential due diligence, such as PPSR title searches, to ensure the vehicle isn't stolen or carrying hidden debt from a previous owner. This gives you dealership-level security and professional paperwork management while allowing you to hunt for the best possible price in the private market.