You've finally found the perfect rig to expand your fleet, but by the time the big bank finishes its third round of paperwork, the seller has already handed the keys to someone else. It's a gut-wrenching way to miss a growth opportunity. Securing heavy vehicle finance shouldn't feel like a part-time job or a race you're destined to lose. You deserve a process that values your time, avoids hidden balloon payments, and gets you behind the wheel without the soul-crushing wait times.

We're here to help you master the complexities of heavy vehicle lending so you can secure competitive funding without the typical bank-runaround. This 2026 guide simplifies the path to fast approvals while ensuring you preserve your vital working capital. We'll explore how to leverage the permanent $20,000 instant asset write-off and identify which finance structures, from chattel mortgages to finance leases, offer the best tax advantages for your specific operation. It's time to scale your fleet with total confidence and leave the bureaucracy in the rearview mirror.

• Learn why choosing the right finance structure, such as a Chattel Mortgage or Finance Lease, is more critical for your long-term cash flow than just chasing the lowest interest rate.

• Discover the "Modern Way" to secure heavy vehicle finance by bypassing big-bank bureaucracy and accessing a panel of over 30 specialised lenders.

• Understand the difference between Low-Doc and Full-Doc application paths to determine which route gets your machinery on the road in the fastest possible timeframe.

• Find out how to maximise your tax position by leveraging structures that allow for GST credits and the permanent $20,000 instant asset write-off.

• Identify why your local bank might decline your application despite your profitability and how a specialist broker bridges the gap in "credit appetite."

•

What is Heavy Vehicle Finance and Why Does Structure Matter?

•

Comparing Finance Structures: Chattel Mortgage, Lease, or Hire Purchase?

•

The Application Process: Getting Your Fleet on the Road Faster

•

Bank vs. Broker: Why the Traditional Route Often Fails Contractors

•

Securing Your Industrial Assets with Motorlend

Heavy vehicle finance is a specialised category of commercial lending designed for assets with a Gross Vehicle Mass (GVM) exceeding 4.5 tonnes. This isn't just about bigger trucks. It's about understanding the industrial cycle of your business. While a standard car loan might work for the family SUV, industrial-scale equipment demands a completely different approach. Standard consumer products lack the flexibility to handle the heavy depreciation, high-intensity usage, and specific tax requirements of a commercial fleet.

When you choose tailored vehicle finance, you're doing more than just buying a machine. You're protecting your cash flow. Matching the loan term to the asset’s effective life is vital. If you fund a trailer over seven years but it only lasts five, you're paying for a ghost. A well-structured deal ensures your repayments align with the revenue the asset generates. This keeps your business liquid and ready for the next contract. It’s about making the debt work for you, not the other way around.

We see a huge range of equipment on Australian worksites. While most people think of logistics, heavy finance covers far more than just the highway haulers. It includes:

•

Logistics: Prime movers, trailers, and rigid trucks for interstate freight.

•

Earthmoving: Excavators, dozers, and graders for civil construction and mining.

•

Agriculture: Tractors and harvesters for the farming sector.

By using a Finance lease or a chattel mortgage, businesses can acquire these high-value tools without draining their bank accounts. This diversity is why a one-size-fits-all loan fails. An excavator has a different value curve than a prime mover, and your finance should reflect that.

In this space, the equipment usually acts as the primary security for the loan. This is a massive advantage compared to unsecured business loans. Because the lender has a claim on the truck or excavator, they take on less risk. This lower risk translates directly into more competitive interest rates for you. Securing heavy vehicle finance is often easier because the asset itself does the heavy lifting for the application.

Asset-backed lending is a finance arrangement where the value of the physical equipment secures the debt, providing the lender with a safety net and the borrower with lower borrowing costs. It’s a straightforward, honest way to fund growth without putting your personal home or other business assets on the line.

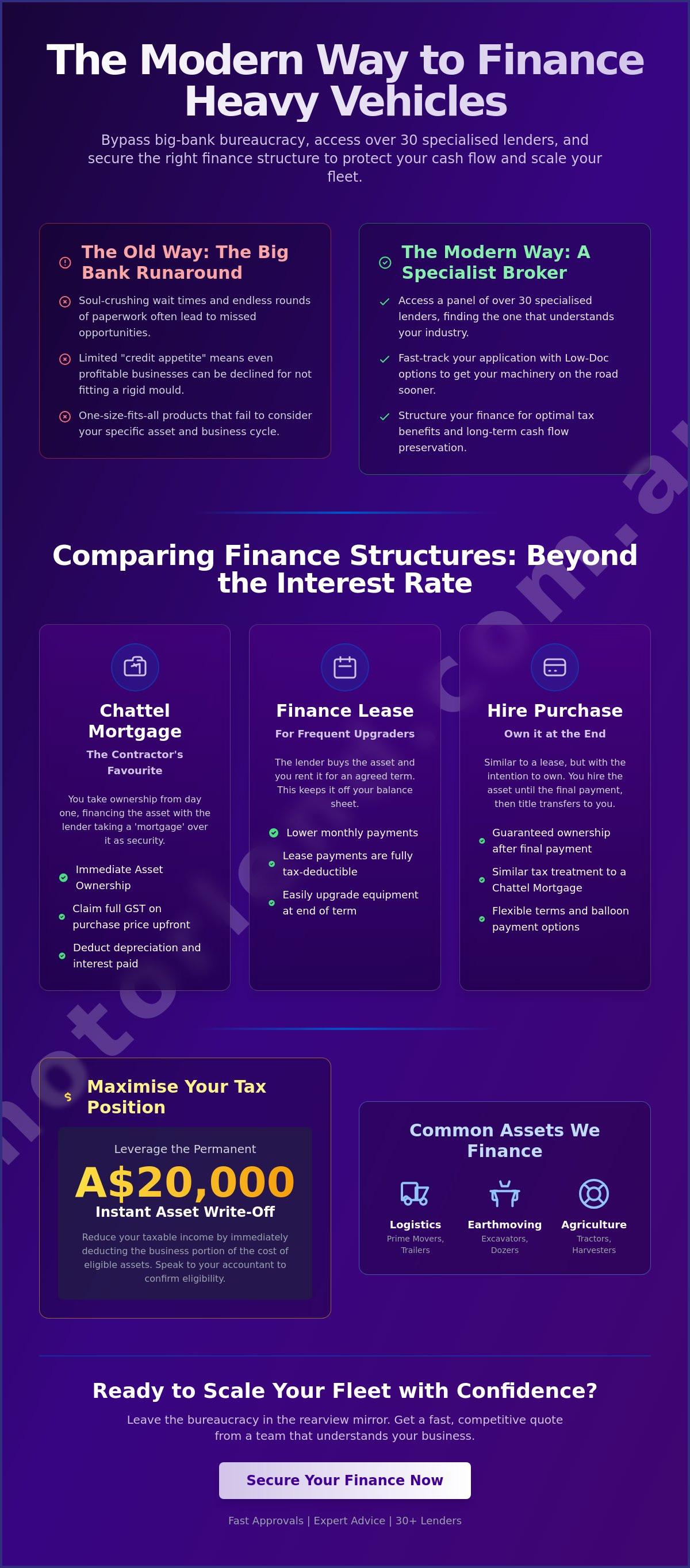

Choosing the right way to pay for your equipment is just as vital as the engine specs. In the world of heavy vehicle finance, three main structures dominate the market. Each has a different impact on your tax returns, your balance sheet, and your monthly cash flow. Understanding whether you want to own the asset immediately or simply pay for its use can save you thousands over the term of the loan. It’s not just about the interest rate; it’s about how the debt interacts with your business model.

For most contractors and small businesses, the Chattel Mortgage is the go-to choice. You take ownership of the vehicle from the moment you drive it away. Because you own it, you can generally claim the full GST on the purchase price in your next Business Activity Statement (BAS). This provides an immediate cash injection that helps with initial operating costs. If your business operates on a cash-basis accounting system, this structure is particularly effective for matching your tax deductions to your actual spending. It’s a direct, no-nonsense way to get gear on the road while keeping your accountant happy.

A Finance Lease works differently. The lender retains ownership, and you pay for the right to use the asset. This is a smart move if you want to upgrade frequently and avoid the hassle of disposing of old machinery. On the other hand, a Commercial Hire Purchase is built for those who want to keep the asset long-term. You hire the vehicle for a set period and take ownership once the final payment is made. Both options allow for balloon payments, which are lump sums paid at the end of the term. These residuals lower your monthly commitments, keeping more money in your pocket for daily operations. If you aren't sure which path fits your 2026 growth plan, you can explore tailored finance options that match your specific cash flow needs.

GST treatment varies significantly between these options. With a Chattel Mortgage, GST is claimed upfront. With a lease, you generally claim GST on the monthly rental payments. As of June 2026, the ATO continues to offer the permanent A$20,000 instant asset write-off, which makes the Chattel Mortgage even more attractive for smaller assets or specific components. Always check with your accountant to see how these structures interact with your specific tax bracket and reporting requirements. Choosing the wrong structure can lead to a nasty surprise at tax time, so getting it right from day one is essential.

Waiting weeks for a credit decision is a luxury most Australian contractors don't have. When a prime mover or a high-spec excavator hits the market, the window of opportunity is often measured in days, not weeks. Streamlining heavy vehicle finance requires a clear, methodical approach that cuts through the noise. By following a proven process, you move from "just looking" to "keys in hand" without the usual stress of bank-runarounds.

The journey starts with a clear budget. You need to determine your maximum monthly commitment and the specific asset requirements before you start shopping. Once your budget is set, the process follows these critical steps:

•

Step 1: Identify the asset and confirm its GVM and intended use.

•

Step 2: Choose the right documentation path based on your business history.

•

Step 3: Partner with a broker to organise your paperwork and tender the deal to multiple lenders simultaneously.

•

Step 4: Receive and review your letter of offer, checking for hidden fees or restrictive conditions.

•

Step 5: Settlement occurs, funds are transferred, and you take delivery of the vehicle.

Your documentation path determines how much of your life story you need to share with the lender. Low-Doc paths are the express lane. They are ideal for established businesses with a clean ABN history and good credit. Usually, you'll only need your ID, ABN, and a declaration of income. This is the fastest way to secure heavy vehicle finance for straightforward replacements or additions.

Full-Doc applications are required for more complex scenarios, such as massive fleet expansions or when you're chasing the absolute lowest market rates available. You'll need to provide recent Business Activity Statements (BAS), profit and loss statements, and potentially tax returns. While it takes more effort, it provides the lender with the confidence to approve larger sums or better terms.

The used machinery market in Australia is incredibly competitive. If you're heading to an auction or a private sale, showing up with "pre-approval" gives you the upper hand. It tells the seller you're a serious buyer with the backing to close the deal immediately. Without it, you're just another person making enquiries while someone else drives away with your equipment. A specialist broker slashes the time-to-settlement by managing the back-and-forth with the lender's credit team, ensuring your file doesn't gather dust on a desk.

Walking into your local bank branch to ask for heavy vehicle finance often feels like a waste of a good morning. You've been with them for a decade. You're profitable. Yet, they still say no. This happens because of "credit appetite." Banks have internal quotas that change without notice. If they've already lent too much to the transport sector this quarter, they'll tighten their criteria, regardless of your business's strength. They have one set of rules and one limited product suite. If you don't fit their narrow box, you're out of luck.

A broker operates differently. Instead of one product, you get access to a panel of over 30 lenders. This includes specialised industrial financiers that the big banks don't want you to know about. Some people worry that brokers are expensive. It's a common myth. While brokers receive a commission, the interest savings from a more competitive tender usually far outweigh the cost. More importantly, the right structure can save you thousands in tax. You aren't just paying for an application; you're paying for a specialist who knows how to pitch your business to the right credit team.

Big banks love to tie everything together. They'll try to link your business debt, your equipment finance, and even your family home under one umbrella. This is called cross-collateralisation. It's dangerous. If one part of your business hits a rough patch, the bank has leverage over everything you own. Brokers help you diversify your lending. We "silo" your equipment finance so the truck or machinery is the only security. This protects your other assets and gives you the freedom to move lenders if a better deal comes along later. Maintaining this separation is a cornerstone of smart wealth management; for instance, Quantum Brokers provides specialised guidance on structuring home loans to ensure they complement, rather than complicate, your commercial borrowing power.

Not all lenders are created equal. Some financiers have a massive appetite for "yellow gear" like excavators and dozers but won't touch a prime mover. Others specialise in long-haul logistics but avoid agricultural machinery. A broker knows exactly which credit teams are hungry for your specific asset type. This insight prevents unnecessary credit enquiries that can damage your score. If you're ready to see what a specialised approach looks like, you can apply for heavy vehicle finance today and get a response that actually moves your business forward.

Having a single point of contact who understands the difference between a rigid truck and a tipper is invaluable. You won't have to explain your industry to a junior bank clerk who has never stepped foot on a worksite. For more information on how we handle these industrial-scale deals, check out our Commercial and Heavy Machinery Finance page for a deeper dive into our specialised process.

Motorlend isn't your average finance broker. We're the Australian specialists in heavy vehicle and commercial asset finance who actually understand what happens on a worksite. We've seen the stress of contractors being treated like a number by big banks. That's why we built the "Modern Way" to buy. Our digital-first approach slashes approval times without losing the human touch. When you need a decision, you talk to an expert, not a chatbot or a call centre in another time zone.

Our expertise goes far beyond just prime movers. Whether you're looking for civil earthmoving gear, specialised mining equipment, or agricultural machinery for the upcoming harvest, we have the lender relationships to make it happen. We don't just look for the lowest rate. We find tailored solutions that match your specific growth goals. This ensures your finance structure supports your cash flow rather than choking it. Securing heavy vehicle finance has never been this straightforward.

Managing a business is demanding. We know that when the weekend finally rolls around, you want to switch off. Motorlend provides a complete asset solution that covers both your commercial needs and your lifestyle balance. We can fund leisure assets like boats, motorbikes, or caravans with the same speed and transparency we apply to your fleet. There's a massive convenience in having one point of contact for every vehicle in your life. If you're planning a trip away from the job site, check out our RV and Motorhome Finance options to get your downtime sorted as efficiently as your work day.

The Australian industrial landscape moves fast. You can't afford to be held back by bureaucratic headaches or lenders who don't understand your credit appetite. Motorlend offers national service capability across all of Australia, from the city centres to the most remote mining hubs. We're ready to help you scale your operations with a quick quote and a transparent process that puts you in control. Every minute your gear isn't on the road is a minute it isn't earning. We get that.

Don't let a slow bank stop your momentum. It's time to experience a finance partner that values your time as much as you do. Our team handles the heavy lifting in the background so you can stay focused on the job at hand. Get your heavy vehicle finance moving with Motorlend and see the difference a specialised, modern approach makes for your business.

Scaling your operations shouldn't be stalled by red tape or rigid bank policies. We've explored how the right structure, whether it's a chattel mortgage for upfront GST benefits or a finance lease for fleet flexibility, protects your cash flow. By moving away from the traditional bank model, you gain access to a wide panel of specialist Australian lenders who actually understand the transport, construction, and agricultural sectors. This specialised knowledge is the difference between a fast approval and a missed opportunity.

Securing heavy vehicle finance is about finding a partner who values your time as much as you do. Our fast, no-fuss approvals are designed specifically for busy business owners who need to move gear onto the job site yesterday. Stop the paperwork runaround and start making the most of the permanent A$20,000 instant asset write-off. Apply for tailored heavy vehicle finance today and let our team handle the bureaucracy while you focus on the road ahead. Your next big growth phase is just a few clicks away.

Yes, you certainly can. While traditional banks often demand two years of clean trading history, many specialist lenders offer "startup" paths for businesses with an ABN active for as little as 12 months. You might need a slightly larger deposit or a clear business plan, but it’s a standard way for new contractors to get their first rig on the road without waiting years for a bank's approval.

Interest rates depend on your business history and the age of the equipment. As of June 2026, established businesses with strong credit typically see rates between 6.89% for chattel mortgages. If you're a newer operator or have a limited credit history, rates for heavy vehicle finance can range from 7.49% depending on the lender's risk assessment.

A balloon payment is entirely optional. It’s a strategic tool used to lower your monthly repayments by leaving a lump sum to be paid at the end of the term. If your goal is to own the asset outright with no remaining debt, you can choose a "fully amortised" loan. This pays the balance down to zero over the term, which is often preferred for assets you plan to keep for a decade or more.

Not necessarily. Many established businesses can secure 100% finance, meaning you keep your cash in the bank for fuel and wages. If you're a new startup or have a complex credit history, a deposit of 10% to 20% can be a game-changer. It lowers the lender's risk, which often results in a faster approval and a more competitive interest rate for your deal.

You can finance machinery from both dealers and private sellers. Dealer sales are generally faster because the paperwork is standardised. For private sales, the lender will usually require an independent inspection and a PPSR check to ensure the title is clear and the asset is in good nick. A broker manages these extra steps so you don't have to worry about the logistics of the sale.

Upgrading is a straightforward process. You can trade in your current vehicle and use the trade-in value to pay out the existing loan. Any remaining balance can often be rolled into a new heavy vehicle finance agreement. This allows you to keep your fleet modern and take advantage of better fuel efficiency or newer technology without waiting for a five-year loan term to expire.

It’s a completely different beast. Standard car loans are consumer products for personal vehicles, whereas heavy vehicle finance is a commercial facility for assets over 4.5 tonnes GVM. Commercial lending offers tax-effective structures like finance leases and chattel mortgages that aren't available to individual car buyers. The credit assessment also focuses on your business's ability to generate income rather than just your personal salary.

The tax advantages are one of the main reasons ABN holders choose this structure. You can generally claim the full GST on the purchase price in your next BAS, which provides an immediate boost to your cash flow. Additionally, you can claim the interest on the repayments and the asset's depreciation as tax deductions. As of 2026, the permanent A$20,000 instant asset write-off remains a powerful incentive for eligible smaller equipment purchases.