What if waiting weeks for a bank manager's approval is actually the most expensive part of your next project? We know the drill. You've got a job ready to go, but your capital is tied up and the traditional lenders are buried in red tape. It's frustrating to watch site gear sit idle while you're stuck decoding the difference between a finance lease and a chattel mortgage. Getting the right construction equipment finance shouldn't feel like a second job.

You deserve a clear path to scaling your fleet without draining your working capital. This guide breaks down how to secure fast access to the machinery you need while keeping your monthly repayments predictable and your cash flow healthy. We'll show you how to maximise tax deductions like the $20,000 instant asset write-off available for the 2026 income year. From navigating the current 4.35% RBA cash rate environment to picking the most tax-effective loan structure, you're about to master the art of fleet expansion.

• Keep your cash where it belongs—in your business—by using smart financing to cover site gear while preserving capital for wages and materials.

• Navigate the 2026 landscape of construction equipment finance by comparing chattel mortgages and finance leases to find your perfect tax-effective fit.

• Streamline your approval process with our fast-track checklist, ensuring your BAS and P&L statements are ready for a quick "yes" from lenders.

• Learn why modern firms are ditching traditional banks for specialist brokers who actually know the difference between a backhoe and a bobcat.

Cash flow is the lifeblood of any Aussie site. While it's tempting to think that buying a machine outright is the "cleanest" way to grow, it often creates a dangerous bottleneck. If you drop $200,000 on a new excavator today, that's $200,000 you can't use for materials, subbie wages, or fuel when a bigger project lands next month. In the current market, liquidity is your best competitive advantage. Construction equipment finance allows you to keep that capital in the bank, ready for emergencies or growth opportunities that require immediate funding.

Modern fleet management also demands constant upgrades. With 2026 safety and emissions standards becoming stricter across civil projects, running older, less efficient gear can actually disqualify you from certain tenders. Financing lets you swap out older models for compliant, high-tech machinery without a massive capital hit. Most importantly, this is typically structured as asset-based lending. This means the equipment itself acts as the primary security. It protects your personal assets, like the family home, from being tied up in your business's yellow-gear acquisitions.

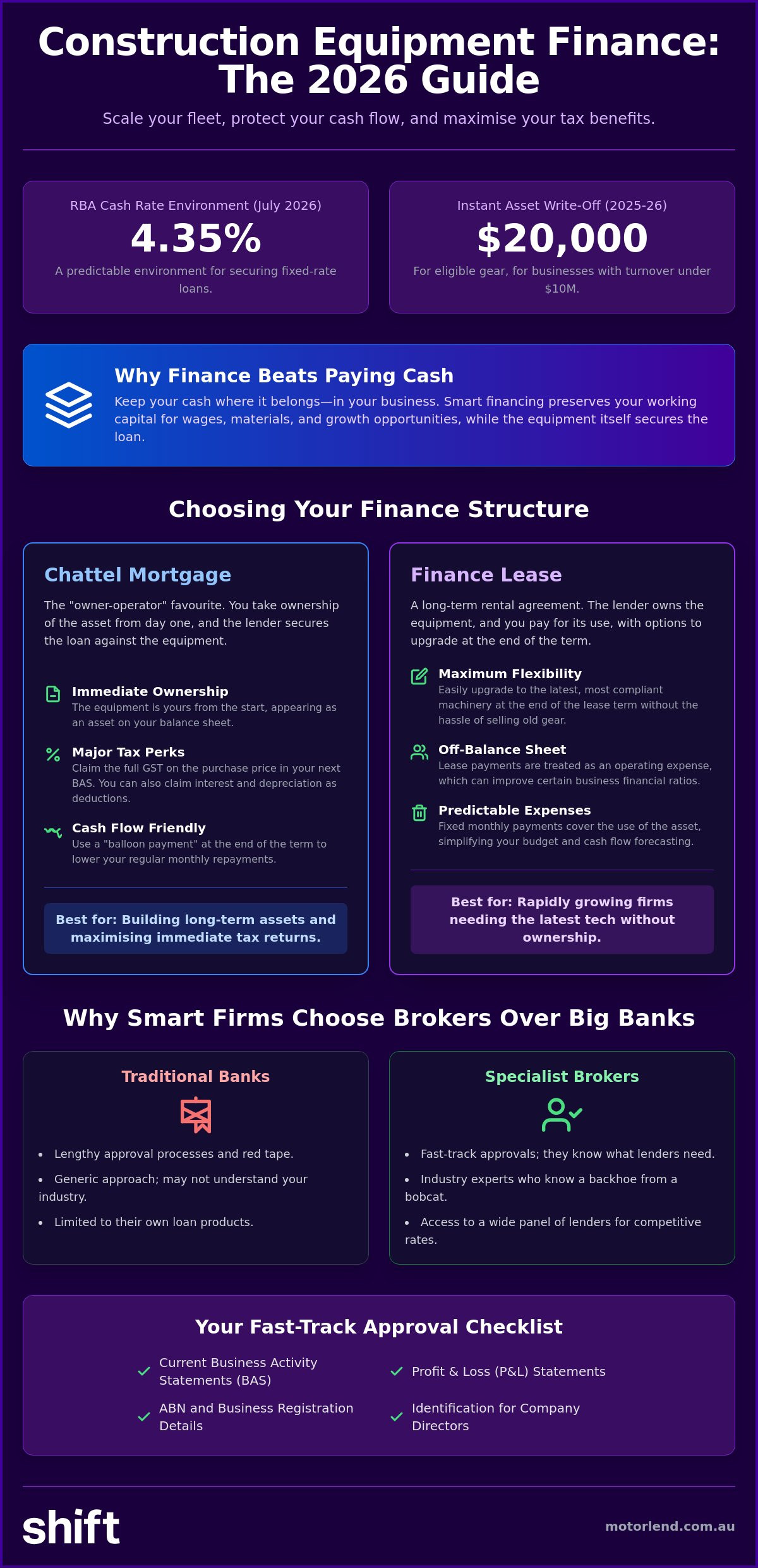

The Reserve Bank of Australia has held the cash rate at 4.35% as of July 2026, creating a predictable environment for businesses looking to expand. With a surge in specialised civil infrastructure projects across the country, the demand for high-performance gear is peaking. Using commercial finance means you can scale your fleet in days, not months. You can say yes to that new contract immediately, knowing your monthly repayments are fixed and manageable.

Your accountant likely hates seeing large cash outlays for depreciating assets. For the 2025-2026 income year, small businesses with a turnover under $10 million can still access the $20,000 instant asset write-off for eligible gear. Financing allows you to stay under these thresholds while still getting the best machinery on site. By spreading the cost, you can often claim the interest and depreciation as deductions, making construction equipment finance a far more tax-effective strategy than burning through your hard-earned cash reserves.

Choosing the right structure for your construction equipment finance is just as important as picking the right machine for the job. Not all loans are built the same. Pick the wrong one, and you could be stuck with a repayment schedule that doesn't match your project cycles. Most Aussie tradies gravitate toward the Chattel Mortgage because it puts you in the driver's seat from day one. You own the asset immediately, while the lender simply secures the loan against the machinery itself. It's a straightforward, "no-nonsense" approach that mirrors how most successful small businesses operate.

If you prefer to keep your fleet fresh and avoid the hassle of selling old gear, a Finance Lease might be the better play. This works like a long-term rental where the lender owns the equipment, and you pay for the right to use it. At the end of the term, you can often upgrade to the latest model. This keeps your site compliant with the latest safety standards without the headache of ownership. For a deeper dive into how these liabilities look on your books, you can consult official government finance guides to see which reporting style suits your business size.

This is the heavy hitter for a reason. One of the biggest perks is the ability to claim the full GST on the purchase price in your very next BAS period. It provides an immediate cash flow injection that other structures can't match. You can also organise "balloon payments" at the end of the term. This strategically lowers your monthly costs, keeping more cash available for fuel and subbie wages while you're out on site.

Operating leases and Commercial Hire Purchases (CHP) offer different levels of flexibility for specialised needs. Operating leases are perfect for high-tech gear that might be obsolete in a few years; you use it for the project and hand it back. In the 2026 market, with the cash rate sitting at 4.35%, many firms are opting for fixed rates to ensure their construction equipment finance remains predictable. If you're ready to see which structure fits your project pipeline, you can start your application online in just a few minutes.

Getting a "yes" on your construction equipment finance application shouldn't feel like pulling teeth. While traditional banks might leave you hanging for weeks, modern lenders are looking for specific indicators of health that allow them to move fast. In 2026, the focus has shifted toward real-time data. Having your latest Profit & Loss statement and Business Activity Statements (BAS) ready is non-negotiable. Lenders also scrutinise the credit history of both the business and its directors; a clean record is the fastest way to secure competitive rates.

The type of gear you choose also dictates your terms. While used machinery might have a lower sticker price, new equipment often comes with lower interest rates because it represents less risk. Effectively managing heavy asset value is a core part of modern fleet strategy. If you've got a signed contract or a "Letter of Intent" for an upcoming project, bring it to the table. It proves your ability to service the loan and can significantly speed up the approval process for construction equipment finance.

Speed is everything when a new job is on the line. Have these items organised before you start the conversation:

• Current ABN and ACN details.

• Recent tax returns (usually for the last two years).

• Detailed equipment quotes from a reputable dealer.

If you've been trading for more than two years with a solid asset base, you might qualify for "Low Doc" loans. These require less paperwork and focus on your recent BAS and bank statements to prove income, allowing for a much faster turnaround.

Many firms fall into "analysis paralysis" at the dealership. They wait until they've found the perfect rig before thinking about the money. This is backwards. You should apply for pre-approval before you start shopping. It gives you a clear budget and puts you in a stronger position to negotiate with sellers. Don't let a "no" from one bank stop you; different lenders have different appetites for specific machinery types. Getting your finance sorted first ensures you're ready to pounce when the right gear becomes available.

Big banks often treat you like a number. They have rigid, "one-size-fits-all" rules that don't always work for the gritty reality of the construction industry. If your business doesn't fit their exact box, you'll get a "no" faster than you can finish your smoko. This is where a broker changes the game. By working with a wide panel of lenders, a broker ensures that one bank's rejection is simply a stepping stone to another lender's approval. It's about finding a home for your construction equipment finance that actually understands your balance sheet.

Brokers also bring specialised industry knowledge to the table. Most bank managers wouldn't know a bobcat from a backhoe. A specialist broker understands the resale value of your gear and the specific demands of your site. This expertise helps them structure your commercial finance to match your project's cash flow. They get your gear on-site while the big banks are still trying to find a time for a preliminary meeting. Speed and agility are the hallmarks of a good broker; they know that every day your gear isn't on-site is a day you're losing money.

Nobody has time to sit on hold for forty minutes. When you work with a broker, you get a single point of contact who actually knows your business name and your goals. Motorlend organises the heavy lifting—the paperwork, the lender negotiations, and the constant follow-ups—so you can stay focused on the project. We clear the bureaucratic path so you can scale your fleet without the stress of managing construction equipment finance yourself.

Securing heavy machinery finance in this market requires a tailored approach that considers the current 4.35% cash rate and your specific growth goals. Don't let red tape slow your business down while jobs are waiting. If you're ready to expand your fleet and keep your cash flow healthy, get a fair dinkum quote from the Motorlend team today and get your next rig on-site faster.

Scaling your business in 2026 requires more than just hard work; it demands a smart approach to capital. By choosing construction equipment finance over a massive cash outlay, you protect your liquidity and stay ready for the next big tender. Whether you opt for the ownership benefits of a chattel mortgage or the flexibility of a finance lease, the goal remains the same: getting the right gear on-site without the financial stress. You've seen how a bit of preparation and the right structure can transform your balance sheet.

Ditch the bank's hold music and rigid policies. As specialist commercial finance brokers with national coverage, we help Aussie tradies bypass the red tape. We provide access to over 40 leading lenders, ensuring you get a deal that actually fits your project pipeline and cash flow needs. We handle the heavy lifting in the background so you can focus on the job at hand.

Ready to scale your fleet? Apply for a no-obligation quote today. Your next big rig is closer than you think. Let's get to work and get your business moving.

Yes, you can absolutely finance used machinery. Most lenders are happy to fund second-hand gear provided it meets certain age and condition requirements. Generally, if the machine is expected to be under 15 years old by the end of the loan term, you'll have access to plenty of competitive options. It's a brilliant way to get reliable site gear without the steep depreciation costs of a brand-new model.

Approval for a Chattel Mortgage can happen in as little as 24 to 48 hours when your documents are ready. Because the equipment itself serves as security, lenders can move much faster than they would with a traditional unsecured business loan. Having your recent BAS and ABN details organised allows us to skip the bank queues and get a "yes" before your next project starts.

A balloon payment is a lump sum you agree to pay at the very end of your loan term. By deferring a portion of the principal, you significantly lower your monthly repayments throughout the life of the loan. This strategy is a lifesaver for construction equipment finance because it keeps more cash available for daily operational costs like fuel, subbie wages, and materials.

You typically need an active ABN and GST registration to access the most competitive commercial finance rates. Being GST-registered is also a huge advantage because it allows you to claim the GST on the purchase price back in your next BAS period. While some niche lenders might consider non-registered businesses, being registered opens up a much wider panel of over 40 lenders and better terms.

Yes, start-ups can secure equipment finance, though you might need to provide a larger deposit or additional security. Lenders generally look for at least six to twelve months of trading history; however, some specialist lenders focus specifically on helping new firms get their first rig. Providing a signed contract for upcoming work or a letter of intent can also help prove your business's ability to handle the repayments.