What if the biggest barrier to your business growth isn't your balance sheet, but the dread of another "bank-says-no" email? It's a common frustration for the 2.7 million businesses currently trading across Australia. You know you need that new truck or specialised machinery to hit your 2026 targets, but the thought of waiting weeks only to be rejected is enough to stall any expansion plans. We get it. Managing cash flow while trying to scale is a high-wire act, especially with the RBA cash rate sitting at 4.35% and lenders tightening their belts. Finding the right commercial finance shouldn't feel like a second full-time job.

You deserve a clear path to the assets you need without the bureaucratic headache. This guide breaks down exactly how to secure funding for everything from heavy machinery to vehicle fleets while keeping your cash flow healthy. We'll demystify the confusion between chattel mortgages and leases, explain how to make the most of the $20,000 instant asset write-off, and show you why non-bank lenders are becoming the go-to for savvy operators. Here is everything you need to know to fuel your business growth in the current Aussie market.

• Learn how commercial finance keeps your working capital where it belongs—in your business—while you secure the latest assets.

• Discover the 'Asset Life' strategy to ensure you aren't still paying for equipment long after it has stopped making you money.

• Find out how to assess your cash flow to pick the perfect balance between monthly repayments and balloon amounts.

• Understand why the 'Multi-Lender Advantage' is the fastest way to get a 'yes' when the big banks aren't playing ball.

Think of commercial finance as the high-octane fuel in your business tank. At its core, it is a specialised funding structure designed to help you acquire essential assets without wiping out your bank balance. Instead of handing over a massive lump sum for a new truck or a piece of heavy machinery, you spread the cost over time. This approach keeps your working capital liquid, which is vital in 2026 as the Australian economy navigates an RBA cash rate of 4.35%.

Using Commercial finance allows you to preserve cash flow for day-to-day operations, marketing, or emergency repairs while still operating with the latest, most efficient equipment. It is a world away from a standard personal car loan. If you hold an ABN, you unlock access to lending products specifically built for business growth. These often feature different tax treatments and repayment structures that a personal loan simply cannot offer.

In the commercial finance space, most agreements are asset-backed. This means the equipment you are buying serves as the security for the loan. Because the lender has a tangible asset to fall back on, they often provide more favourable interest rates compared to unsecured business loans. Having a valid ABN is your ticket to these deals. It tells lenders you are a professional operator, opening doors to specialised rates and higher lending limits that help you scale faster.

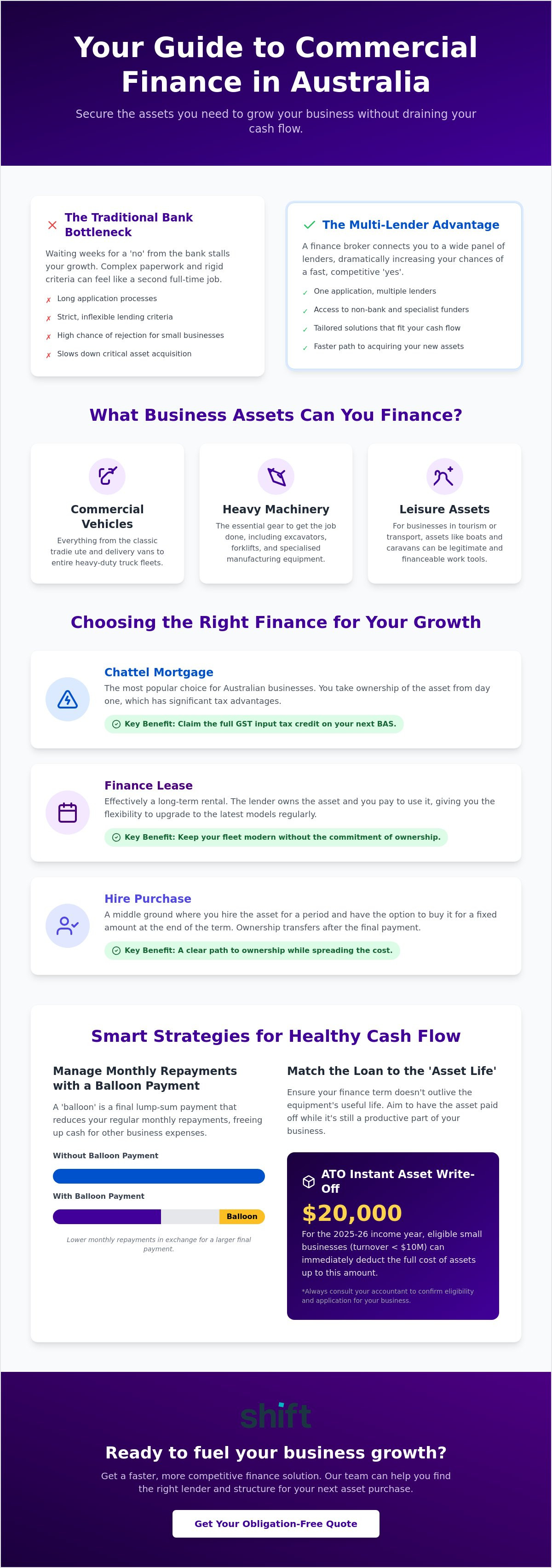

What can you actually fund? The list is broader than many business owners realise. We regularly help Aussie operators secure the gear they need to get the job done:

This includes the classic tradie ute, delivery vans, and heavy-duty truck fleets.

Excavators, forklifts, and specialised manufacturing equipment for the workshop.

For some businesses, a boat or caravan is a legitimate work tool. This might be for tourism, site accommodation, or specialised transport.

Choosing to finance these assets rather than buying them outright means you can upgrade more often. You stay competitive. You stay efficient. Best of all, you do it without the stress of a drained savings account.

The journey of commercial finance in Australia follows a fast-paced path: the vault, the broker, and finally, your driveway. We act as the vital bridge between wholesale lenders and your specific business needs. Unlike traditional property-based lending that often gets bogged down in slow valuations and complex liens, our process focuses on the speed and utility of the asset. This efficiency is critical when you need a new ute or excavator on-site yesterday to fulfill a fresh contract.

Success depends on matching your loan term to the 'Asset Life' of your equipment. You don't want to be making repayments on a delivery van that has already reached its use-by date. To keep your monthly overheads manageable, many savvy operators use balloon payments. A balloon payment is a final lump sum paid at the end of the loan term that significantly reduces your regular monthly repayments. Researching Australian business finance options shows how these structures can be tailored to your specific cash flow requirements. If you're ready to see what's possible, you can start your application online in minutes.

Choosing the right structure changes your tax position and ownership rights. A Chattel Mortgage is the go-to for many because you own the asset from day one, allowing you to claim the GST upfront. For those who prefer a modern fleet without the long-term commitment, a Finance Lease allows you to use the equipment for a set period before upgrading. A Hire Purchase acts as the middle ground; you use the asset while paying it off, with ownership transferring to you once the final payment is made.

Tax rules in 2026 remain a powerful incentive for growth. Small businesses with an aggregated turnover of less than $10 million can still access the $20,000 instant asset write-off for the 2025-2026 income year. How you handle GST and depreciation depends entirely on your chosen loan structure. Because every business has a unique financial footprint, you should always consult your accountant before signing a contract to ensure the setup aligns with your tax strategy.

Scaling a business in Australia requires more than just ambition. It takes a calculated approach to how you fund your next move. Navigating the commercial finance market is simpler when you follow a logical path. First, you must identify the asset's primary use. If it's 100% for business, your tax benefits differ significantly compared to a split with personal use. Next, assess your current cash flow. This helps you decide on a monthly repayment that doesn't choke your operations, alongside a balloon amount that makes sense for the asset's future value.

Once your strategy is clear, gather your "Big 3": your ABN details, current identification, and basic financial statements or bank feeds. Having these ready turns a slow process into a fast one. Finally, engage a specialist broker. While the "big four" banks have their place, they often lack the flexibility required for agile businesses. A broker scans the wider market to find rates and terms that actually fit your industry. For more detailed advice on managing these decisions, the Australian Government business finance portal offers excellent resources for small business owners.

Don't be blinded by shiny "dealer finance" offers at the showroom. These often come with hidden administration fees or rigid terms that don't suit a growing company. A low interest rate can be a trap if the upfront fees or early exit penalties are sky-high. Focus on the total cost of the loan over its entire life. For a deeper dive into these specifics, read our guide on Business Vehicle Finance in Australia: The 2026 Guide to Smarter Asset Growth.

Waiting for years of savings to buy heavy machinery is a recipe for falling behind. Competitors using newer, more efficient technology will underbid you every time. This is the "Opportunity Cost" of staying small. Using commercial finance to upgrade your fleet or equipment now means you can take on bigger contracts immediately. If you're ready to jump on a new opportunity, you can get your quote started today.

Going direct to your bank for commercial finance often feels like trying to fit a square peg in a round hole. Traditional banks usually have one "box" of criteria. If your industry is currently out of favour or your business structure is slightly non-standard, they simply say no after making you wait for weeks. We don't work that way. We understand that every Aussie business has a different story and different needs.

Our "Multi-Lender Advantage" gives you immediate access to a wide panel of lenders. Some specialists love the construction sector; others prefer transport, logistics, or medical equipment. We find the specific lender that already wants to say yes to your industry. This saves you from multiple credit hits and the frustration of constant rejections. By the time you talk to us, we have already done the legwork to find your best match.

In 2026, speed is the only currency that truly matters for growth. Our digital approval process is built for the modern age, often getting your gear on the road in days rather than weeks. We handle the heavy lifting and the complex paperwork in the background. You stay focused on your customers. We keep the entire experience jargon-free because you have better things to do than decode banking legalese or corporate double-speak.

We bring specific expertise to machinery finance for the construction and transport sectors. Our team understands that a truck or an excavator isn't just a vehicle; it's your primary source of income. We know why a tradie needs a specific GVM rating or why a truckie needs a particular trailer setup to stay profitable. We speak your language and we know your gear.

Our application process is fast, simple, and entirely online. You can apply for commercial finance from your cab, the job site, or your home office. Join the thousands of Australian businesses we have helped get moving over the years. Whether you are looking to add one ute or an entire fleet, our human experts are ready to help you secure the funding you need to scale without the stress.

Scaling your operations in a shifting economy requires more than just hard work; it demands a smart approach to how you fund your future. You now understand that commercial finance is a strategic tool to keep your cash flow liquid while you put the latest gear to work. By choosing the right structure and avoiding common showroom traps, you position your business to take on bigger contracts and outpace the competition.

At Motorlend, we specialise in getting Australian tradies and transport operators moving without the typical bank runaround. Our team provides access to a massive panel of lenders and uses a fast, jargon-free digital process to secure your vehicle or heavy machinery funding. We do the heavy lifting in the background so you can stay focused on the job at hand.

Don't let a "no" from a big bank stall your momentum. Secure your business growth and apply for tailored commercial finance today. It's time to get your business the assets it deserves and start scaling with confidence.

A chattel mortgage provides you with immediate ownership of the asset from the day you pick it up, while a commercial hire purchase means the lender technically owns the equipment until you make the final payment. Most Australian businesses prefer a chattel mortgage because it typically allows you to claim the full GST amount on the purchase price in your next Business Activity Statement (BAS). It is often the simplest way to get gear on your books quickly.

Yes, you can get commercial finance as a start-up, provided you have a valid ABN and a solid credit history. While some traditional lenders want to see two years of trading history, we work with specialist lenders who offer low-doc options for new businesses. This means you can get the tools or vehicles you need to start earning immediately without waiting years to build up a massive paper trail of tax returns.

You don't always need a deposit to secure funding for a new ute, truck, or piece of machinery. Many lenders offer 100% finance to established ABN holders, allowing you to preserve your cash for operating expenses or unexpected repairs. If your credit history is a bit thin or the asset you are buying is highly specialised, a small deposit can sometimes help secure a more competitive interest rate and faster approval.

Approval for commercial finance in Australia is significantly faster than a standard home loan, often taking just 24 to 48 hours. Our digital application process bypasses the old-school bank queues, meaning you can often move from application to settlement in less than a week. The speed usually depends on having your documents ready to go and choosing a lender that understands your specific industry and asset type.

To get started, you will usually only need your ABN, a current driver's licence, and access to your recent bank statements via secure bank feeds. For larger or more complex machinery loans, a lender might occasionally request your most recent financial statements or a profit and loss report. We aim to keep the paperwork to a minimum so you can stay on the tools while we handle the heavy lifting in the background.