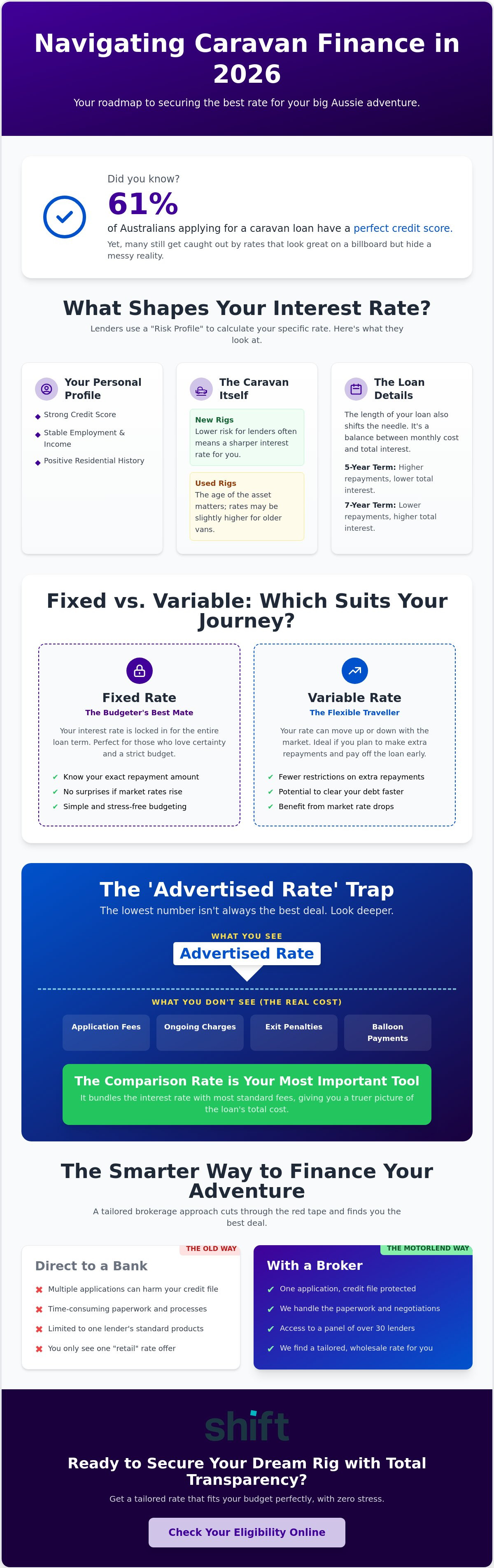

Did you know that 61% of Australians applying for a caravan loan have a perfect credit score, yet many still get caught out by caravan finance rates that look great on a billboard but hide a messy reality? It's completely normal to feel a bit of anxiety when you're staring at a sea of financial jargon, hidden balloon payments, and confusing comparison rates. You want to be planning your next big trip to the Kimberley, not losing sleep over whether you're being overcharged for your freedom. Dealing with banks can feel like a slow trek through thick scrub, especially when the paperwork starts piling up and the fine print gets blurry.

We're here to clear the air and make things simple. You're going to discover how to navigate the 2026 lending market to secure the most competitive deal for your next adventure. We'll break down the latest data from major lenders, explain why the lowest advertised number isn't always the best deal, and show you how a tailored approach cuts through the red tape. By the time you've finished reading, you'll have the confidence to lock in a low rate with total transparency and zero stress.

• Understand the 2026 Australian lending landscape and how it shapes the total cost of financing your next big road trip.

• Discover how lenders use your unique risk profile and credit history to calculate your specific caravan finance rates.

• Learn why the comparison rate is your most important tool for spotting a genuine bargain and avoiding "advertised rate" traps.

• Uncover the hidden fees and charges, such as application costs and exit penalties, that often lurk in the fine print.

• Find out how a tailored brokerage approach gives you access to wholesale rates while keeping your credit file protected during the search.

Caravan finance rates are simply the interest charged on a loan specifically for your recreational vehicle. Think of it as the price you pay to get your rig on the road sooner. In 2026, these rates aren't just a random number; they're a carefully calculated percentage based on the current economic climate and how lenders view the "lifestyle asset" market. A vital step in your research is understanding the annual percentage rate (APR), as this includes both the interest and the standard fees that can sneak up on you.

The Australian economy has shifted recently, and this has changed how lenders approach caravan loans. Banks are looking closer at household budgets, but there's still a massive appetite for helping Aussies get outdoors. Secured caravan loans remain the gold standard for savvy buyers. By using your caravan as security, you're telling the lender the loan is lower risk, which usually unlocks a much better deal. The 2026 market trend is firmly focused on "risk-based pricing," where your personal financial health dictates the specific rate you're offered.

Choosing your rate type is about balancing certainty with flexibility. A fixed rate is your best mate if you love a strict budget. You'll know exactly what's leaving your account every month for the life of the loan. No surprises. No stress. Variable rates, however, can be a great shout if you plan on paying the loan off early. They often come with fewer restrictions on extra repayments, allowing you to clear the debt faster if you have a win. While vehicle finance for your daily car might be straightforward, caravan finance rates reflect the unique nature of leisure assets, often sitting slightly higher due to different depreciation scales.

Lenders don't just pick a number out of a hat. They use a "Risk Profile" to decide your specific caravan finance rates. This profile is a digital snapshot of your financial life. It looks at your credit score, your job stability, and even your residential history. A recent ASIC review of motor vehicle finance highlighted how important it is for consumers to receive fair outcomes, showing that being informed about what drives these numbers is your best defence against overpaying. When you understand the "why" behind the rate, you're in a much stronger position to negotiate.

The caravan itself plays a massive role in the final percentage. Lenders generally prefer brand-new caravans because they have a higher resale value and come with manufacturer warranties. This lower risk for the bank often translates to a sharper interest rate for you. If you're buying a used van, the age of the asset matters. For rigs older than five years, some lenders might nudge the rate up slightly to cover the potential for depreciation. You can often offset this by offering a larger deposit, which lowers the lender's overall exposure and keeps your monthly costs down.

Your credit history is the foundation of your finance offer. A clean record with no missed bills tells a lender you're a safe bet. However, income stability is just as vital. Lenders want to see that you can comfortably manage the repayments without breaking a sweat. This is where a broker adds real value. We don't just pass on a bank's standard offer; we package your application to highlight your financial strengths. We essentially "pitch" your case to a panel of over 30 lenders to find the one that values your profile the most. If you're planning to upgrade your tow vehicle at the same time, exploring vehicle finance alongside your caravan loan can sometimes simplify the process. Ready to see what your profile can actually unlock? You can check your eligibility online in just a few minutes.

The length of your loan also shifts the needle. While a 7-year term makes your monthly repayments smaller, it might carry a slightly higher rate than a 5-year term. It's all about finding that "sweet spot" where the rate is low, but the monthly commitment still fits your lifestyle perfectly.

Don't get blinded by a flashy headline. A low number on a billboard doesn't always mean a cheap loan. When you're hunting for the best caravan finance rates, you need to look past the "advertised" interest and focus on the total cost of the deal. The goal is to avoid the frustration of thinking you've found a steal, only to realize the fees are eating your holiday budget. Transparency is everything in the 2026 market, and knowing what to look for puts you back in the driver's seat.

By law, Australian lenders must show a comparison rate. This number includes the base interest plus most upfront and ongoing fees. It's the most honest way to compare different offers side-by-side. Imagine Lender A offers 6.5% but charges a $500 application fee and $15 a month. Lender B offers 6.9% with zero fees. Lender B might actually be the cheaper rig over the life of the loan. It's about the bottom line, not just the base percentage. Always look for the number in brackets; that's the one that actually matters for your bank account.

A balloon payment, or residual, is a lump sum you pay at the very end of your loan term. It's a popular choice because it drops your monthly repayments significantly. This keeps more cash in your pocket for fuel and site fees while you're on the road. However, you pay interest on that balloon amount for the entire term. It's a smart move if you plan to upgrade your van in five years and sell the current one to cover the cost. It can be a shock if you haven't budgeted for that final bill, so always weigh up the long-term interest against your current cash flow needs.

Look closely at the fine print for exit penalties. Some banks get cranky if you try to pay your loan off early. They'll slap you with a fee for the privilege of being financially responsible. We think that's rubbish. Before you sign anything, use a caravan loan repayment calculator to run a few different scenarios. Test how a balloon payment or a different term affects your total interest. Ready for a transparent quote without the hidden nasties? Apply for a fast, no-obligation quote and see the real numbers for yourself today.

Finding the right caravan finance rates shouldn't feel like a chore that takes the joy out of your purchase. You've done the research and picked the perfect van; now you need a finance partner who moves as fast as you do. Motorlend isn't a bank. We're a bridge between you and a panel of over 30 of Australia's leading lenders. This means we don't just give you one take-it-or-leave-it offer. We shop around to find the specific loan structure that fits your budget and your new lifestyle.

Most people don't realise that banks often offer brokers "wholesale" rates that aren't available to the general public. When you walk into a local branch, you're usually stuck with their retail pricing. We use our industry relationships to access sharper deals, often with more flexible terms for leisure assets. Our team does the heavy lifting by comparing these options for you. We look at the fine print, check the fees, and present you with the best fit. It's a professional, streamlined approach that saves you time and potentially thousands of dollars over the life of the loan.

Protecting your credit score is another priority for us. Before we submit a formal application, we perform a "soft touch" credit check. This gives us a clear picture of your eligibility without leaving a permanent mark on your credit file. it's a magnificent way to get a clear view of the market without any risk to your financial standing. Once we know which lender is the best match, we move quickly to get your approval sorted so you can start packing the annex.

The Australian caravan market moves quickly, and waiting for a slow bank approval can mean missing out on the rig you want. We pride ourselves on a stress-free process that cuts through the red tape. You provide the details, and we handle the rest; from the initial quote to the final settlement. This leaves you free to focus on the fun stuff, like mapping out your route or choosing the best camping gear. Don't let bureaucracy stand between you and the open road.

Ready to see what you could save? Apply for your tailored caravan finance quote today and get a step closer to your next big adventure.

You're now equipped with the knowledge to look past flashy advertisements and find a deal that actually works for your budget. By understanding how comparison rates and your personal risk profile influence caravan finance rates, you can avoid the hidden fees that catch so many buyers off guard. The right finance structure shouldn't just be affordable; it should give you the peace of mind to enjoy the open road without a second thought.

At Motorlend, we're ready to turn that itinerary into a reality. With access to over 30 Australian lenders and a team of expert brokers who handle all the paperwork, we make the process fast and transparent. We specialise in quick approvals for both new and used caravans, ensuring you don't miss out on the perfect rig while waiting for a bank to call you back. Our goal is to get you hitched and moving with zero stress.

The horizon is calling, and the perfect van is waiting. Get a Tailored Caravan Finance Quote in Minutes and let our experts handle the heavy lifting. We'll find the sharpest deal for your situation so you can focus on the campfire. See you out there.

A competitive interest rate in the current 2026 market generally starts between 5.67% and 7.00% for secured loans, provided you have a strong credit history. If your credit score is lower or you're opting for an unsecured loan, you might see rates climb higher. It's vital to focus on the comparison rate rather than just the advertised base, as this gives you the true cost of the loan including all those pesky fees.

You can certainly secure finance as a self-employed buyer, and we help business owners do this every day. Lenders typically require a few extra documents, such as your most recent tax returns or business bank statements, to confirm your income is steady. We understand the "low doc" and "full doc" options available in the 2026 market and can match you with a lender that doesn't make you jump through unnecessary hoops.

A secured caravan loan is usually the smarter move if you're looking for the lowest caravan finance rates available. By using the caravan as collateral, you reduce the lender's risk, which almost always results in a lower interest rate compared to an unsecured personal loan. While a personal loan offers more freedom to spend the money on other things, the extra interest cost often makes it a more expensive way to get your rig on the road.

Yes, you can finance a used van from a private seller, and about 49% of Australians choose to buy their rigs this way. We handle the background checks to ensure the caravan doesn't have any hidden debt or history that could cause you trouble later. This gives you the freedom to hunt for a bargain on the private market while still enjoying the professional support and competitive rates of a dealer-style finance package.

Most of our customers receive a formal approval within 24 to 48 hours of submitting their paperwork. We know that a good caravan doesn't stay on the market for long, so our digital process is built for speed and efficiency. Once you've provided the basic details, we do the heavy lifting to get you a clear answer quickly so you can commit to your purchase with total confidence.